Use our loan agreement template to detail the terms of a loan.

Updated July 10, 2024

Written by Sara Hostelley | Reviewed by Brooke Davis

A loan agreement is a legally binding contract between a lender and a borrower that a court can enforce if one party doesn’t follow the arrangement. It establishes the amount the lender is lending and sets other terms, including the repayment schedule and interest.

Use a written loan agreement whenever you lend or borrow money. Here are some situations where you may need to create this document:

When making a loan agreement contract between family members, you should be aware that there can be tax implications. For example, if you lend money without interest, the IRS may charge you tax because it would be below the minimum interest rate required for family loans. This amount is the Applicable Federal Rate (AFR). [2]

Also, if you’re borrowing money from family or friends and don’t have to repay the loan, the IRS will consider this transaction a gift and charge you gift tax if the amount exceeds the yearly maximum. [3]

If you see an exorbitantly high interest rate on a potential loan agreement, you shouldn’t sign it without serious consideration. You may be a victim of a loan shark, which is a lender who preys on individuals and charges the highest legal interest rate possible.

Secured Loans: They require collateral as a precondition for borrowing, typically a home or vehicle.

Unsecured Loans: They don’t require collateral. A borrower promises to repay the amount via a contract.

Variable-Rate Loans: They have an interest rate that changes over time.

Fixed-Rate Loans: They have an interest rate that stays the same for their entire duration.

Payday Loans: They’re short-term and immediate loans with high interest rates.

Your credit score indicates how likely you are to repay a loan. Lenders consider this metric when assessing your loan application.

The higher your credit score, the better chance a lender will want to loan to you. You can obtain your credit score from one of the three major credit bureaus: Experian, Transunion, and Equifax. Once you learn your current credit score, you can understand which interest rates you may qualify for.

Shop around for the best personal loan option. Research and compare lenders based on interest rates, fees, repayment terms, and customer reviews.

You have several options to find personal loans:

Consider obtaining a loan from a family member or friend who has extra money to lend. Even if you know the lender well, it’s still a good idea to get a personal loan agreement in writing.

Lenders may request several documents to verify your information. Gather them in advance so you can present them when lenders request them. Examples of these documents include proof of identity (like a driver’s license or an affidavit of identity), proof of income, bank statements, and rental or mortgage agreements.

Many lenders offer a prequalification process involving a soft credit check that estimates the loan amount and interest rate you might qualify for. Thanks to prequalification, you can preview the potential offers you may get from lenders and narrow them down based on potential interest rates, fees, terms, and amounts.

Note that the prequalification process doesn’t guarantee you’ll get a loan. It also doesn’t require you to accept one.

If you’re satisfied with the prequalification terms, pick one that matches your needs and proceed with the formal loan application. Complete the lender’s application form with accurate information, finalize the documents, and accept the terms.

If you receive loan offers after applying, review them carefully. Pay attention to the loan amount, interest rate, repayment term, and associated fees, and read and understand the fine print. If all the details meet your needs, you can accept the offer and sign the loan agreement.

Follow these steps to notarize a loan agreement:

While most jurisdictions don’t require witnesses to legitimize this document, you may consider getting a notary public to sign it. A notary public will ensure all parties sign the document as themselves and without coercion.

If the title company or lender requires notarization, they will arrange for a notary public to be available at the closing.

A loan contract contains basic details, including the principal amount and interest. Explore some other terms and conditions that you can include within this document:

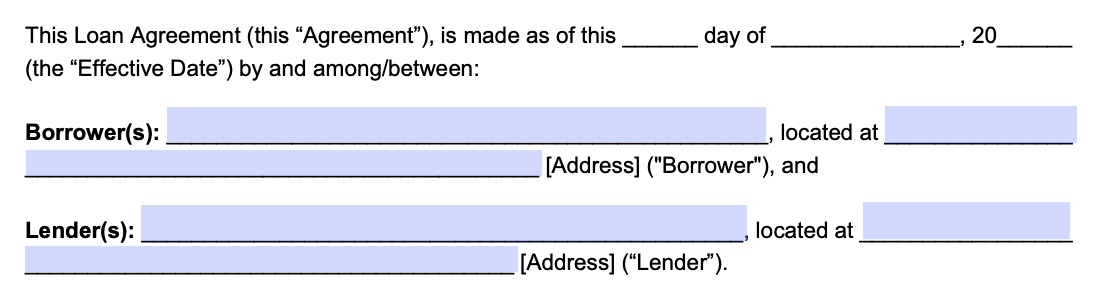

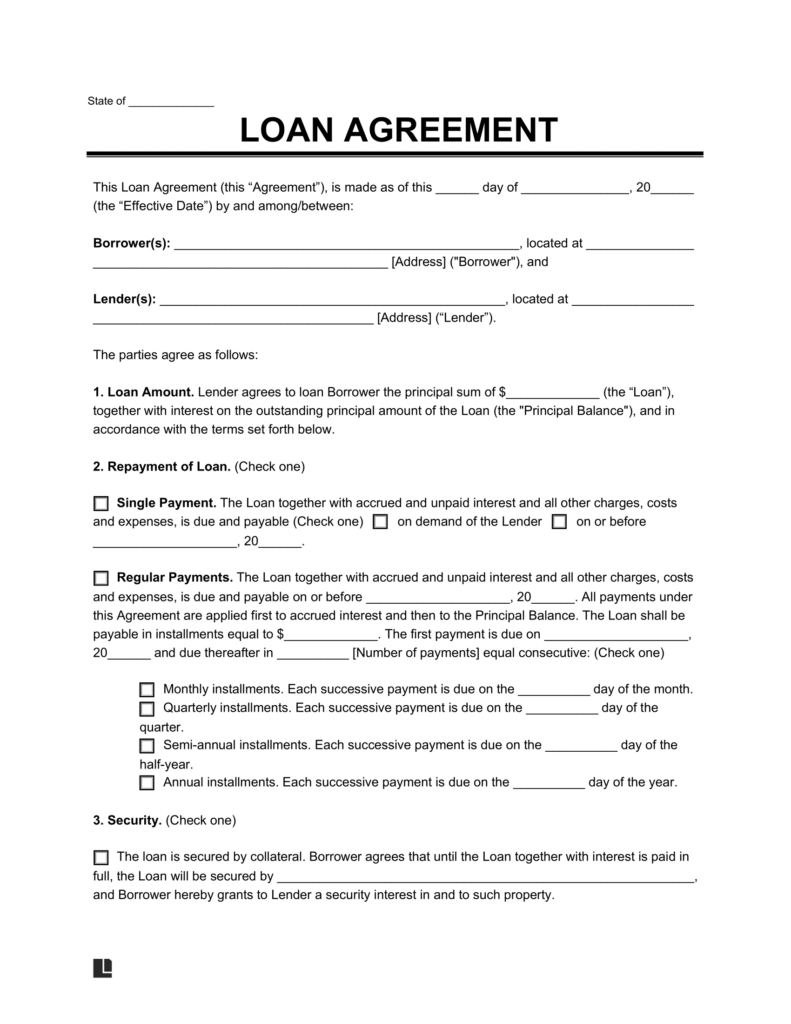

This agreement should detail the lender’s and borrower’s full legal names.

Provide the amount the borrower will be loaning from the lender. This amount is the principal sum. It doesn’t account for the total amount, including accrued interest.

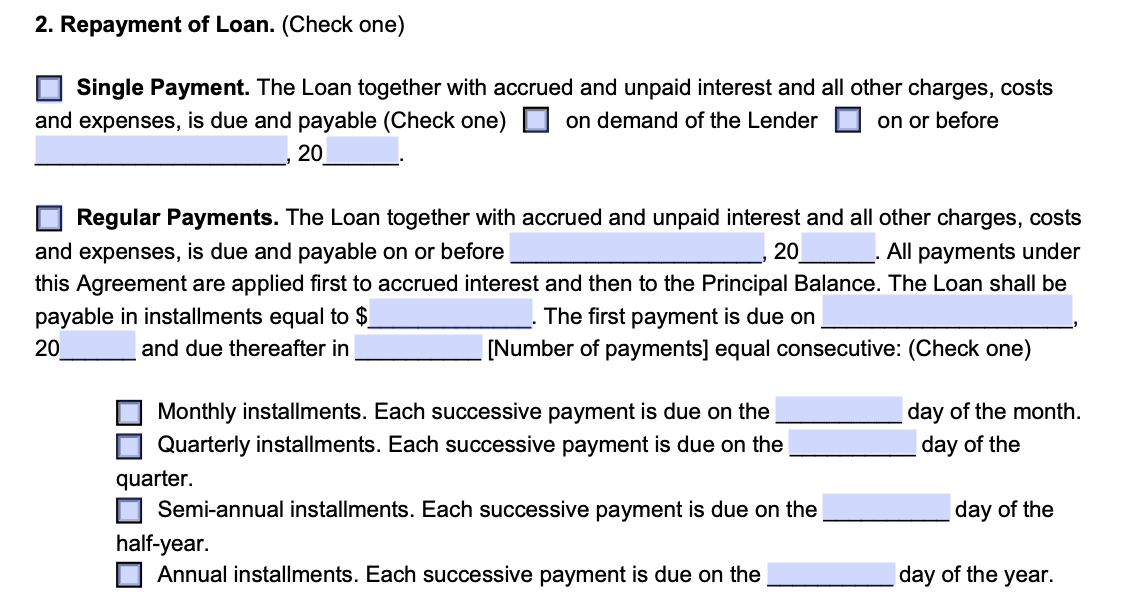

This section is where you must provide the details of the borrower’s loan repayment. The options you choose will have to be mutually agreed upon. You can choose whether the borrower will repay the loan in regular payments or at once.

If you choose regular payments, you must specify the repayment schedule, which can be monthly, quarterly, semi-annual, or annual installments.

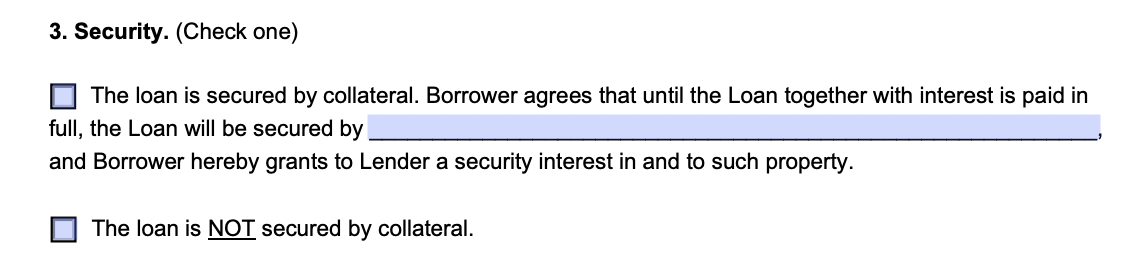

If you want the loan secured, you can include the property the borrower has put up for collateral. Make sure to provide as many relevant details as possible. Both parties must mutually agree upon this collateral for it to be legally valid in court.

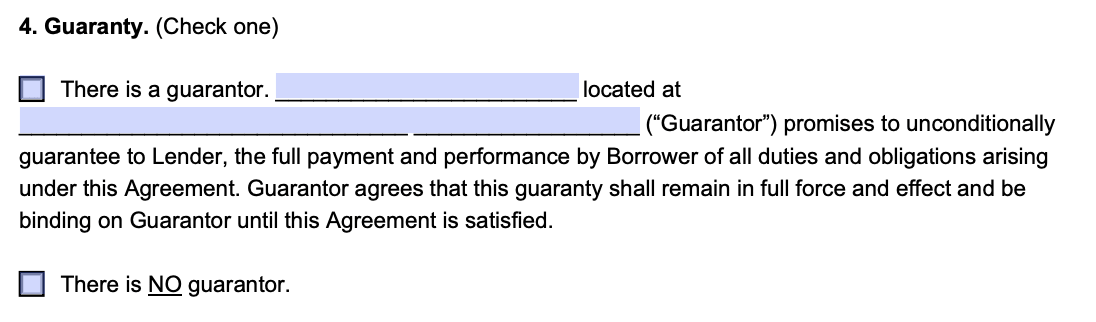

A cosigner or guarantor is optional and protects the lender if the borrower defaults on the agreement. You may require a cosigner if the borrower is in questionable financial standing. The cosigner is someone who jointly signs the agreement with the borrower.

If the borrower defaults and cannot pay back the amount in full, the cosigner is responsible for paying you back the due amount. The cosigner is usually someone in good financial standing or has excellent credit.

You should include the interest rate you will be charging the borrower in a percentage. This interest rate will apply to the principal amount of the loan, and the borrower must agree to this rate.

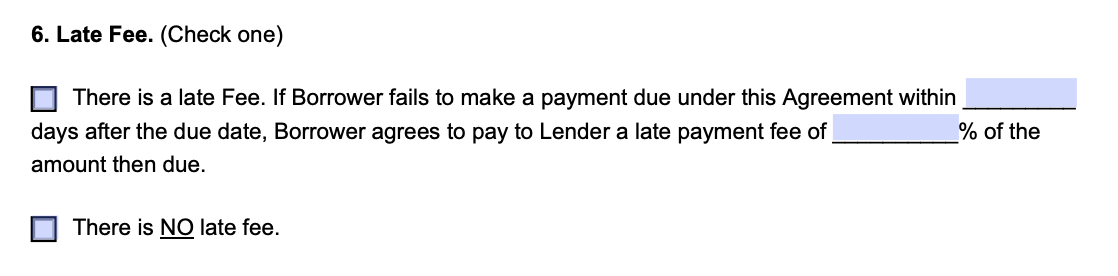

As a lender, you can charge late fees if the borrower does not make a payment in time. Including a late fee can motivate the borrower to make payments on the agreed dates.

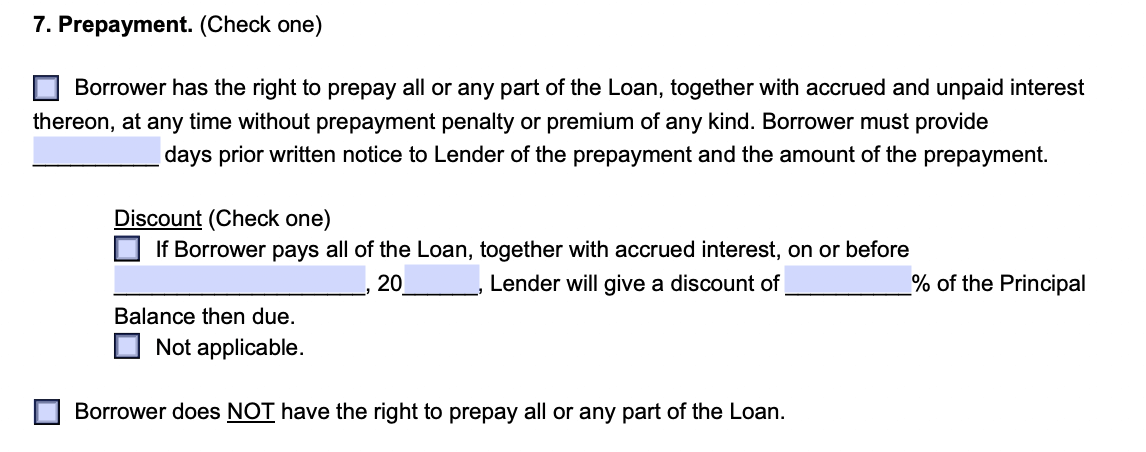

You can include whether penalties or discounts will apply if the borrower decides to pay the loan amount ahead of schedule. Alternatively, you can explicitly state that the agreement does not allow prepayment of the loan.

A penalty can prevent the borrower from paying the loan early and encourage long-term payments. The loan would then accrue more interest, which can be a favorable arrangement for the lender.

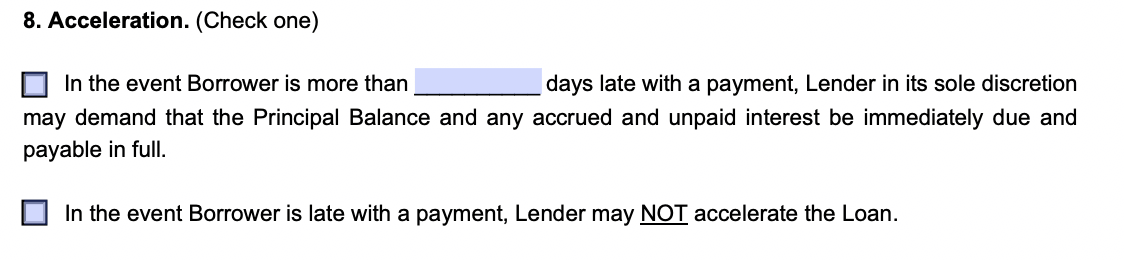

When the borrower cannot repay the loan as the loan agreement details, the borrower has entered into default. It would be best to clarify how the borrower will default in the document. An agreement can say missing one payment causes a default, but a lender may choose to be more lenient.

A default can give you the legal right to accelerate payment. In this scenario, you can make the total loan amount due immediately.

Further terms make up the remainder of the agreement and serve to protect the rights of both parties, and they include any remaining provisions such as:

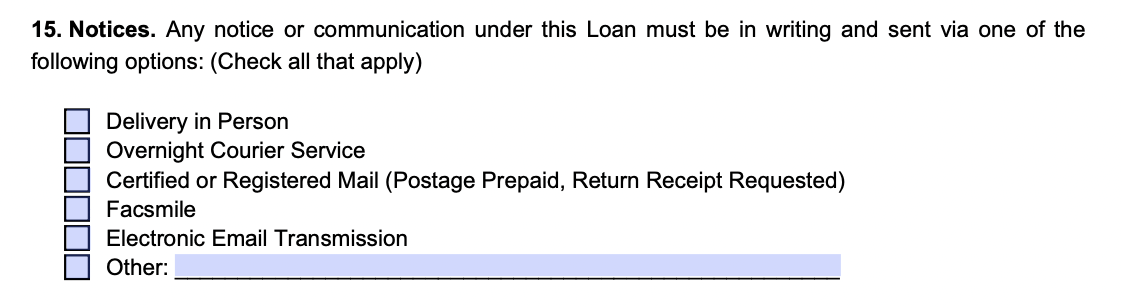

You can establish communication methods so both parties are on the same page. This preparation can prevent either party from claiming they didn’t receive a notice.

Indicate your resident state in the agreement so both parties know which jurisdiction’s laws they must follow.

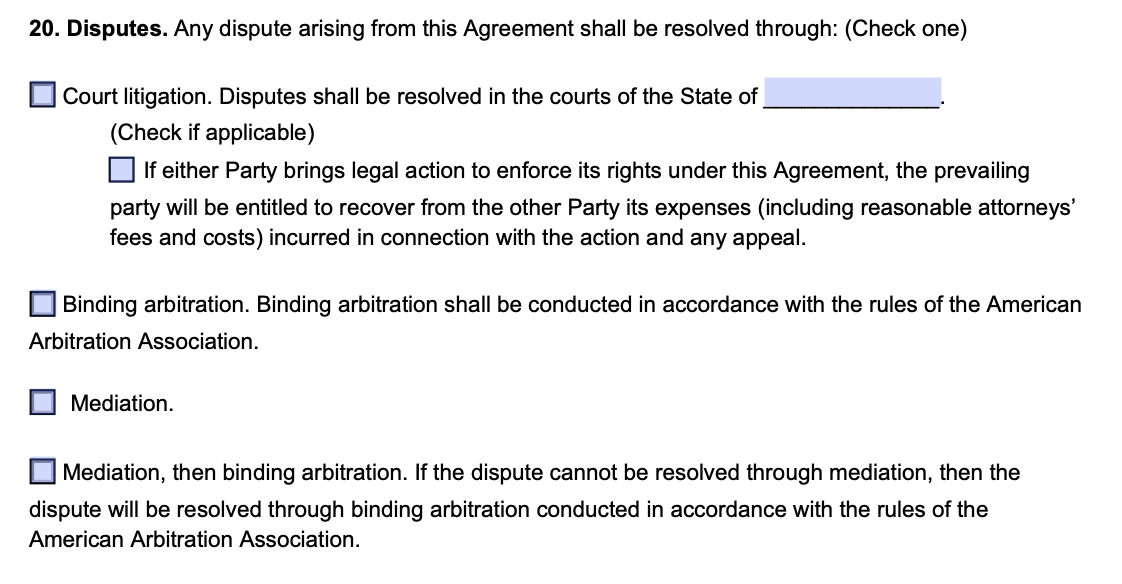

Detail the procedure for how both parties can resolve disagreements. Choose from several options, including court litigation, mediation, and arbitration.

Pursuing court litigation will mean the party who lost the case must pay the other party any costs and fees related to the court process.

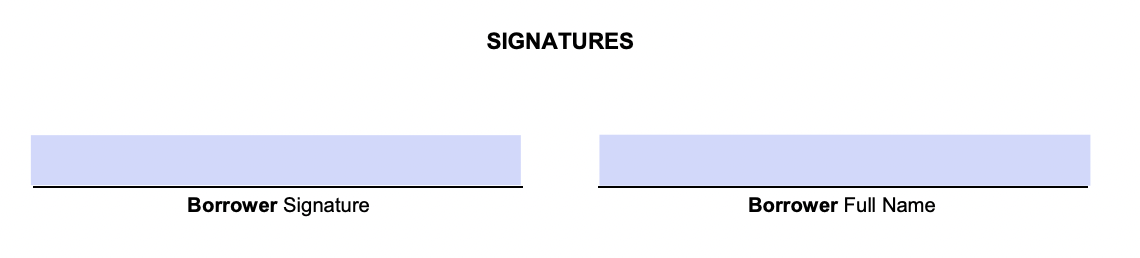

All involved parties in the agreement, including personal guarantors and cosigners, must sign the document.

Here are the documents you may need for a loan-financed purchase and at what stages you may need them:

Download a free loan agreement template as a PDF or Word file below.

A loan agreement and a promissory note are legal documents individuals use when borrowing money from another party. However, promissory notes tend to be shorter and more straightforward. They focus on the borrower’s pledge to repay and contain basic elements like the parties’ names, the loan amount, and the terms.

Loa agreements are more comprehensive since they outline the loan’s terms and conditions in greater detail. They often give both parties more protections, including borrower representations, warranties, and covenants. For more detailed information, you can explore the differences between a loan agreement and a promissory note.

You can cancel this agreement in certain instances. Refer to the original document for termination conditions. You may also be able to cancel the loan if both parties agree to it or if you’re within your jurisdiction’s cancellation period for your specific loan type.

Yes. Consider writing this agreement when borrowing money from or lending to a family member. This agreement can help keep matters objective if you disagree about the loan’s terms later.

Consolidating your loans involves obtaining one sizable loan to pay off all your loans. This way, you only have to make one payment each month. Consolidation may be a reasonable option if you can secure a loan with a low interest rate.

View SourcesLegal Templates uses only high-quality sources, including peer-reviewed studies, to support the facts within our articles. Read our editorial guidelines to learn more about how we keep our content accurate, reliable and trustworthy.

Create Your Loan Agreement in Minutes!