![]()

Homeowners whose mortgage debt is partly forgiven through a loan modification, or "workout," which allows them to continue owning their residence, will receive Form 1099-C reporting the amount of debt discharged. Because the taxpayer kept ownership of the home, there is no gain or loss to be reported.

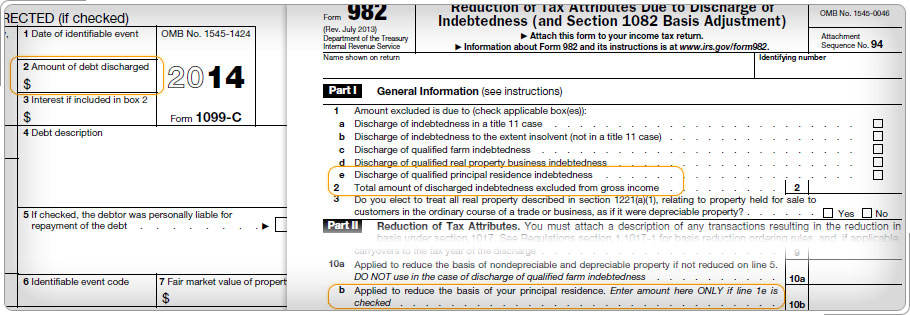

However, if the canceled debt meets the requirements of "qualified principal residence indebtedness," Form 982 must be completed to report the amount excluded from gross income and the reduction of tax attributes. Check box 1e on Form 982. See Publication 4012, Income tab, Capital Loss on Foreclosure, on how to complete Form 982.

Taxpayers who are not personally liable for the debt (nonrecourse debt) do not have ordinary income from the cancellation of the debt unless the lender:

If a lender offers to discount (reduce) the principal balance of a loan that is paid off early, or agrees to a loan modification ("workout") that includes a reduction in the principal balance of a loan, the amount of the discount or the amount of the principal reduction is canceled debt whether or not the taxpayer is personally liable for the debt. The amount of the canceled debt must be included in income unless the exceptions or exclusions discussed earlier apply.

Click Next to continue.